The traditional position:

Capitalised expenditure is placed on the balance sheet for accounting purposes and the associated costs are amortised (or written-down), to reflect the fact that the expenditure will benefit the business over time.

A Company’s P&L Account will show a depreciation expense across each year the asset is in use, which means the business’s profits for that year are an accurate reflection of how the business is performing in reality.

Where intangible assets are concerned, the equivalent of depreciation is known as amortisation.

The most common examples of R&D expenditure capitalised as intangible assets that we see at SeedLegals, are for expenditure on a software platform or a development project that is expected to continue over a number of accounting periods.

How does the deduction work?

The s.1308 deduction allows you to access the full benefit of your R&D tax claim immediately, as this moves your R&D expenditure to your profit and loss account rather than it being on your balance sheet.

This is useful if you have intangible assets, which depreciate. Usually, when tax relief is granted, this is spread over the years the intangible asset benefits the business.

Why would I want to do this?

As mentioned, if you have intangible assets, the R&D tax credit claim will be spread over a number of accounting periods. This means you won’t have access to the full claim amount immediately.

However, you may want to have access to the money straight-away, this is made possible by the s.1308 deduction.

You’ll need to fulfil the criteria below to benefit from this:

- If your company incurs expenditure on research and development (R&D), which is not of capital nature, AND

- Brings the expenditure into account in determining the value of an intangible asset

Here is a worked example:

Say, you had £100K of qualifying spend for R&D purposes. This is sat on your balance sheet as capital expenditure, which means it is amortized and charged to your income statement over 5 years due to normal accounting principles.

In this case, this is how you would received your R&D credit:

Year 1: Tax deductible amortization = £20K

R&D Tax Credit = £6.6K

Benefit = 33%

Year 2: Tax deducitbale amorization = £20K

R&D Tax Credit = £6.6K

Benefit = 33%

Fast forward a couple of years

Year 5: Tax deductible amortization = £20K

R&D tax credit = £6.6K

Benefit = 33%

Total: Tax deductible amortization = £100K

R&D tax credit = £33K

Benefit = 33%

But, if you were to use the s.1308 deduction:

Year 1: Tax deductible amortization = £100K

R&D tax credit = £33K

Benefit = 33%

You would receive the full amount immediately, which can be done on SeedLegals.

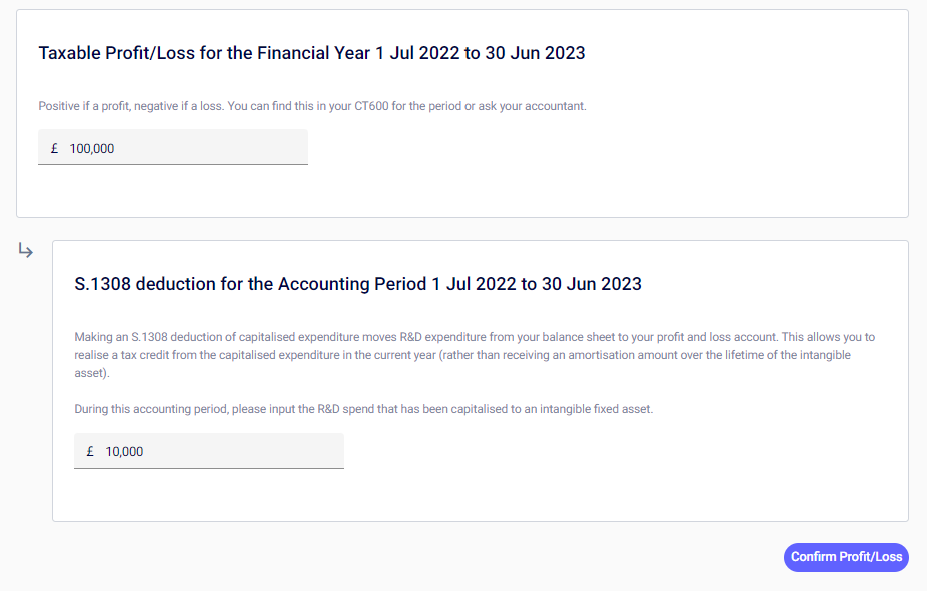

How can you do this on SeedLegals?

Head to the Trading profit or Loss box in your R&D claim, and click on the pen:

You can then enter R&D spend which has been capitalised to an intangible fixed asset, as well as your Taxable Profit/Loss figure. Or leave the bottom box blank if this does not apply to you:

Once that’s filled in, SeedLegals will take this into account and it will populate on your Technical Narrative.

If you have any questions on this or getting ready for your R&D claim, please message us and the team would be happy to help!