The way you actually receive your R&D tax benefit can vary between which scheme you make the claim on, as well as your business’s financial position.

This can be as cash in the bank, a reduction in Corporation Tax or to carry forward (or back) a loss. It can even be a combination of these.

Here, we will discuss how Carrying Forward a loss works with the SME and RDEC scheme and what this means for your tax benefit.

SME Scheme:

Here, you can choose to carry forward your loss and use this to offset it against future profits, get cash money or surrender this for group relief.

This is helpful as this option can mean that you can offset this in the future for better value, but if you are looking for an immediate cash injection - carrying forward this loss might not be for you.

RDEC Scheme:

Without veering into too much detail, RDEC involves 7 steps in order to work out the tax benefit and how this will be received by a company.

This includes offsetting the claim amount against your Corporation Tax for the period you are claiming for (Step 1), or to discharge any other liability of the company to pay a sum to the Commissioners (E.g. VAT) (Step 6). As well as offsetting this against any Corporation Tax which is owed for any other accounting periods (Step 4).

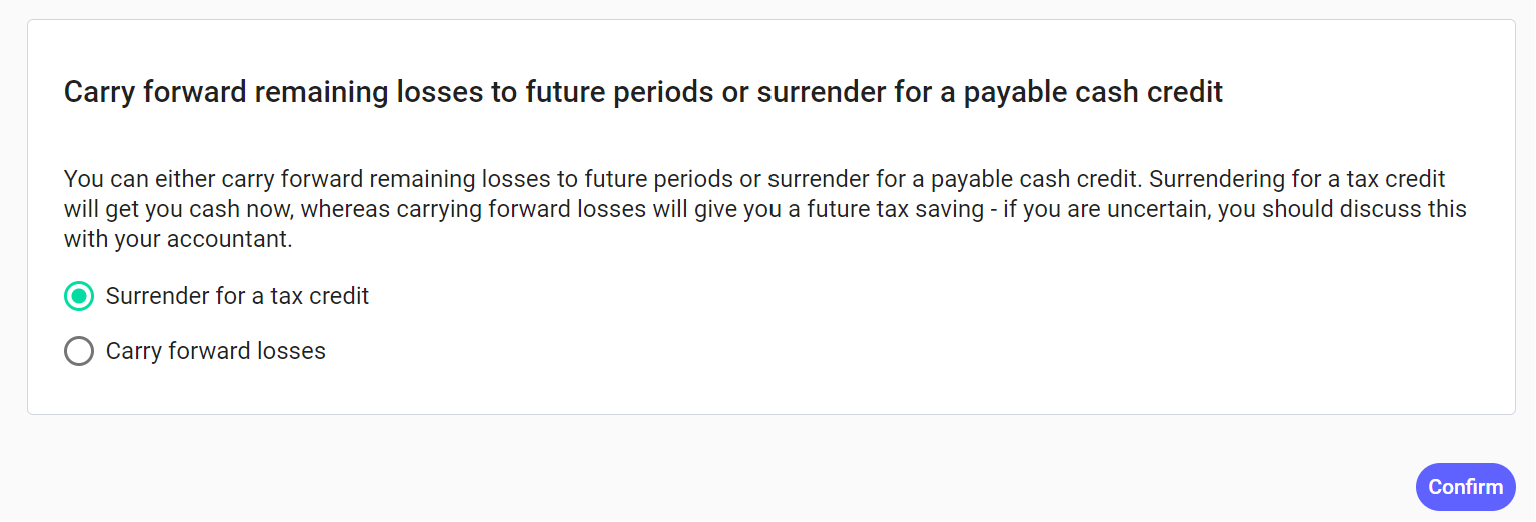

How can I do this on SeedLegals?

If you head to your R&D claim and scroll to the bottom, you should see this below:

Click on the pen, and you will be given the option to surrender for a tax credit, or to carry forward your losses:

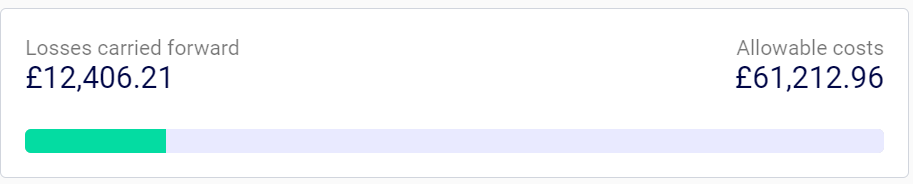

If you select to carry forward your losses, this will then be reflected in the potential cashback bar:

Depending on what you decide, the platform will do the rest for you!

The most efficient way to utilise losses is a complex and often, a rather company specific consideration.

The general rule is, you want to use the losses as early as possible, meaning you use up any losses before they expire.

However, it is also important to consider this in light of the applicable tax rates in each year. As tax rates change over the years, it could make more sense to carry forward the losses into a period where they can claim the losses at the 25% corporation tax rate as opposed to the previous 19% rate.

Due to the complexities involved in this area, we recommend discussing this with your accountant as they will have the best context for your situation and can appropriately advise you accordingly.