1. NIC FAQs

2. Joint NIC Election vs Joint S431 Election

In this guide we explain what the NIC Election is, when it’s needed, who should sign it.

As the NIC Election is a tax form, the following information is a summary of HMRC’s guidance and should not be taken as tax advice, please speak to your accountant for any specific questions or scenarios or email HMRC directly on shareschemes@hmrc.gov.uk.

1. NIC FAQs

- What does NIC mean?

NIC stands for National Insurance Contributions. National Insurance is a tax on earnings and it’s usually deducted by the employer through payroll deductions.

- What is the NIC Election?

It is a tax form that allows a company to legally transfer to the employee the Employer’s Class 1 NIC obligation that arises on employment income from securities options, as well as awards of restricted or convertible securities.

It must be signed by the company and the employee option holder to apply.

- Who is the NIC Election for?

Employees or Directors of the company only who make a gain on exercise of employment related securities (ERS).

- When is NIC payable?

NIC is payable if the exercise of an option is taxable and the shares are Readily Convertible Assets (RCAs) aka shares that can be traded on a recognised investment exchange or for which trading arrangements are in place or are likely to come into place.

- When is an option taxable?

Section 530 of the Income Tax (Earnings and Pensions) Act 2003 (ITEPA) states that there is no income tax or National Insurance contributions charged on the grant of a qualifying EMI option.

If an EMI option is exercised within ten years of the date of grant and there has been no disqualifying event, there will be no income tax or National Insurance contributions due, provided that the employee buys the shares at a price at least equal to the market value they had on the day the option was granted.

However, NIC might arise in instances where EMI options are granted at a discounted price or if they are exercised more than 90 days after a disqualifying event and the shares have risen in value since the disqualifying event.

In summary, an NIC Election is a useful tool for employers who want to manage their National Insurance Contributions more effectively and reduce the risk of unexpected payments. Transferring National Insurance Contributions means that the company will not have unpredictable and uncapped National Insurance payments when there is a chargeable event.

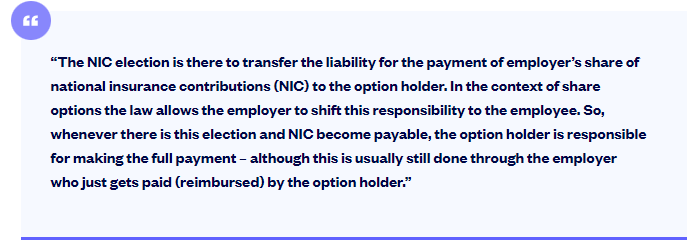

- How can my company recover any NIC payable from the employee?

Employers may recover NICs payable on share options from employees via signing an NIC Election whereby the employer and employee can agree or jointly elect for the employer to transfer the NIC liability onto the employee. Signing the NIC Election ensures any contributions arising from the exercise remains the employee’s responsibility and the option holder is accountable for making the full payment; although this is typically still facilitated through the employer who simply receives reimbursement from the option holder.

HMRC’s guidance states the form of agreement and the arrangements to pay the secondary NICs are matters that will be determined between the employer and the employee. There is no need for HMRC involvement.

If employees exercise an EMI option and an income tax liability arises which is not taxed in full by the employer and paid through the PAYE system, then the employee will need to state the amount of income tax due in their self assessment tax return.

- What if I don’t want to sign the NIC Election?

You do not have to sign the NIC Election if you do not wish to transfer the NIC liability to your employee. However, we strongly encourage companies to sign the Election.

- I already have an approved NIC Election, do I need another one?

Generally if you already have an approved Election for your employee, for example as a result of a previous grant, this can cover future grants too. However, it is best to confirm with HMRC directly.

- I haven't seen the NIC Election before, is this a new requirement?

The NIC Election has always been accessible on HMRC's manual here. It is not a requirement, but we encouraged companies to use the Election.

Recently we have also updated the platform so that when you create a new option grant, the Joint NIC Election document will also be generated for you. You can still approve the grant without signing the Joint NIC Election if you wish .

2. Difference between Joint NIC Election and S431 Election

We often get asked about the difference between the NIC Election and S431 Election. Below is a quick summary of the two and you can also read more about this in our blog post: S431 and NIC tax elections: what are these forms for share option holders?

As always with SeedLegals, we're here to support you every step of the way, so if you get stuck or need a bit of help reach out to your Options Scheme Owner directly or use the chat bubble at the bottom right.