So you've set up either an EMI or an unapproved scheme and now you're ready to get that grant paperwork out of the door - nice!

You'll now need to create the grants for each individual. An Option Grant is the actual paperwork that the employee signs to finalise the granting of a share option (i.e. it is a different document from the Option Scheme). Normally this would be a whole lot of copying and pasting - but now it's super easy on SeedLegals!

Before you begin, we would recommend watching our videos demonstrating how to set-up an option grant. As the processes vary slightly between an option grant with time-based vesting and one with milestone-based vested, we’ve included a video for each below.

Before you begin, we recommend watching the short video below demonstrating how to set-up a time-based option grant

If you intend to grant options vesting based on milestones, we’d suggest you first watch the video below demonstrating how to set this up

Step 1: Work Out How Many Options Each Person Gets

Before you start setting up your option grant, you’ll need to convert any percentage promises into a fixed number of shares.

You may have promised someone "1% of the company" in their contract, but you now need to figure out what that means in actual share numbers. Two important considerations:

- If you've raised investment since making the promise, the grant will have been diluted by that round. Calculate the number of shares based on the share count before that new investment came in.

- Always use the fully diluted total (i.e. including the options pool) when calculating percentages on your cap table, otherwise the maths won't stack up.

Step 2: Create an Option Grant Group

The first thing you'll do is create an option grant group. The platform automatically organises groups by when they're created (e.g. June 2026), the option type (EMI or Unapproved), and how they vest (time-based or milestone-based), so similar grants are kept together.

You'll need to create a group even if you're only granting options to one person, but they're particularly useful when granting to several people at once. There are three main benefits:

- Easier to manage - Get a clear overview of where everything stands: who's signed, who hasn't, and what still needs attention. As you grant more options over time, this keeps things organised and easy to navigate.

- Faster to set up - Set your terms once at group level and every grant in that group will automatically populate with those details. You can still adjust things on an individual basis if needed, but it saves a lot of repetition when terms are similar across the board.

- Simpler to sign - Rather than processing each grant individually, our group signature feature lets you sign and witness every grant in a group in one go.

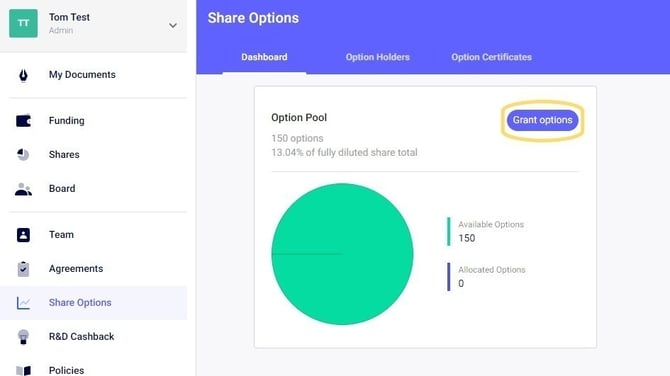

Head to Share Options in the left-hand menu, then select Grant Options. You can start this from either:

- The "Grant Options" button on the ‘Option Holders’ tab, or

- The "Grant Options" button on the Share Options dashboard

Step 2: Add Your Option Holders

After setting up the group, you'll select the people you want to grant options to, either from the list of existing users or by creating a new option holder.

If their details aren't already on the system, add them now by selecting “Add new option holder”, selecting whether they are an individual or a company, then entering their details.

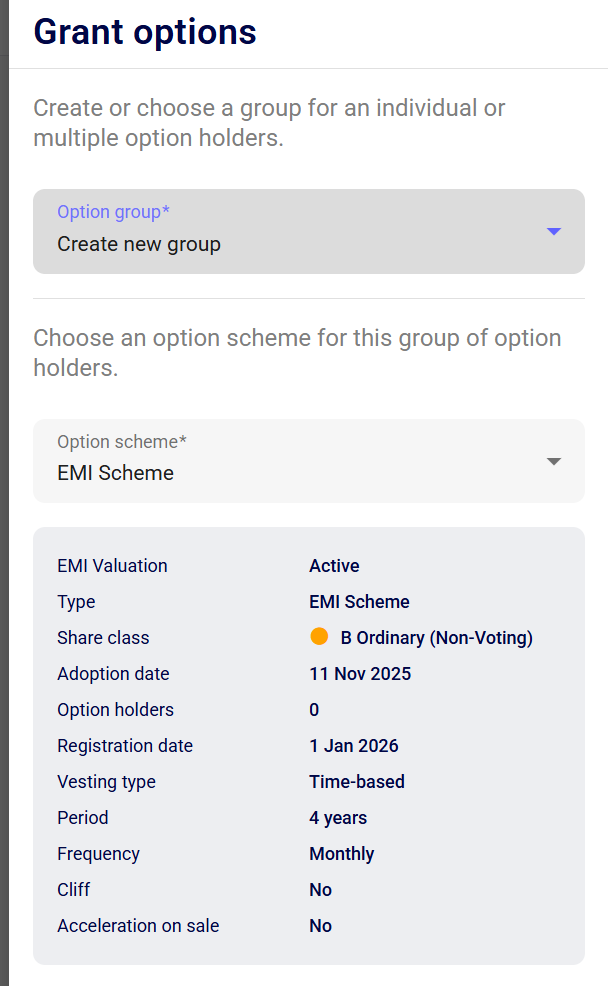

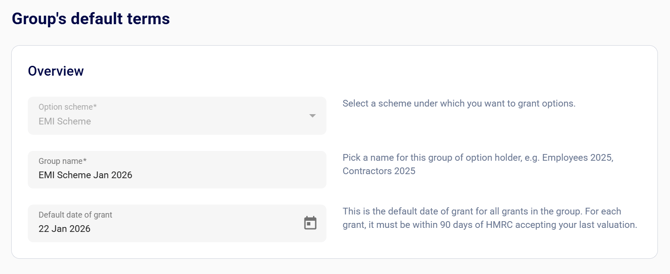

Step 3: Set the Group's Default Terms

You'll now set the default terms that apply across the group. Don't worry, these can be customised for each individual in the next step.

Exercise Price

This is the price the option holder will pay to buy their shares when they exercise their options.

- EMI grants: The platform will automatically pull in the exercise price agreed with HMRC. To avoid income tax on exercise, this should be set to the Actual Market Value (AMV) agreed with HMRC.

- Unapproved schemes: You decide the price. We generally recommend setting it to fair market value, a recent funding round's price per share is a good indicator.

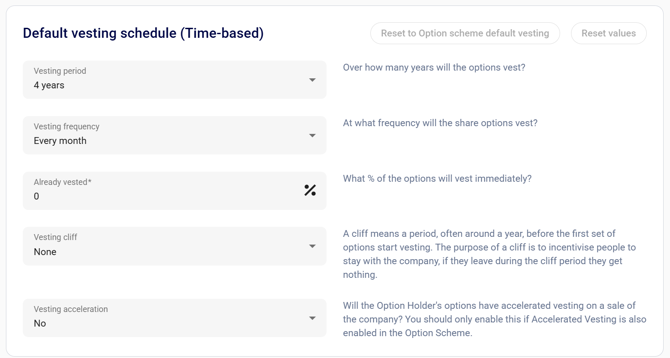

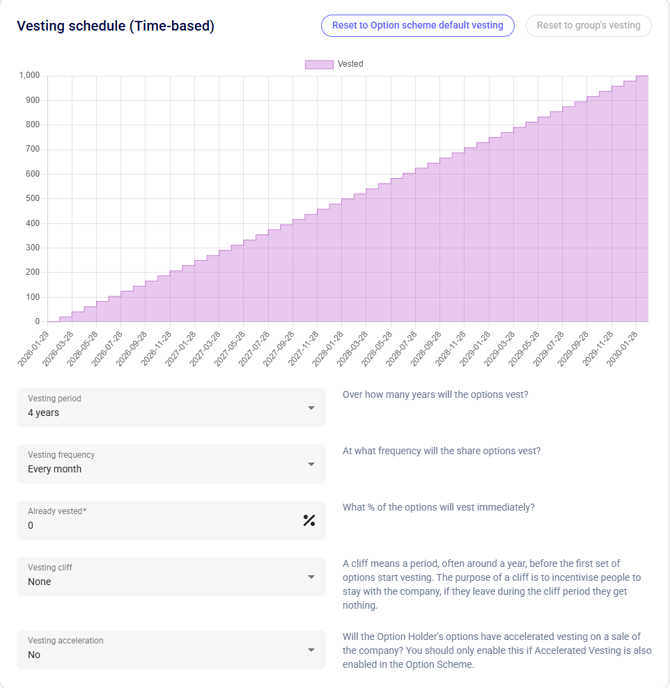

Vesting Terms

You'll set up how and when options are earned:

|

Term |

What it means |

|

Vesting period |

The total time over which options are earned |

|

Vesting frequency |

How often options vest (e.g. monthly, quarterly) |

|

Immediate vesting % |

The percentage that vests straight away |

|

Vesting cliff |

A waiting period before any options vest. If the holder leaves before the cliff ends, they receive nothing. Once they pass the cliff, all options that would have vested during that period are awarded at once |

|

Vesting acceleration |

Whether all options vest immediately upon a company sale. For example, if someone has a 5-year vesting schedule and the company is acquired in year 3, accelerated vesting means all remaining options vest at the point of sale |

|

Acceleration % |

The % of unvested options that vest immediately on a company sale |

|

Acceleration period |

The minimum number of months the holder must work after a sale to benefit from accelerated vesting |

|

IPO acceleration |

Whether options accelerate upon an IPO |

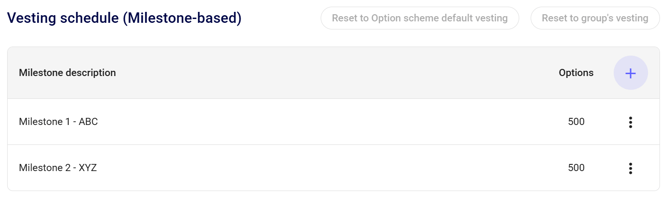

📝 Milestone-based options? You only need to set vesting acceleration as a default term here. Individual milestones are set in the next step.

When you're happy with the defaults, click "Save Group".

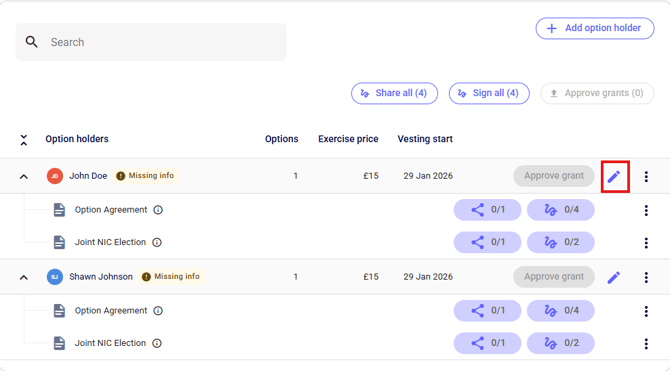

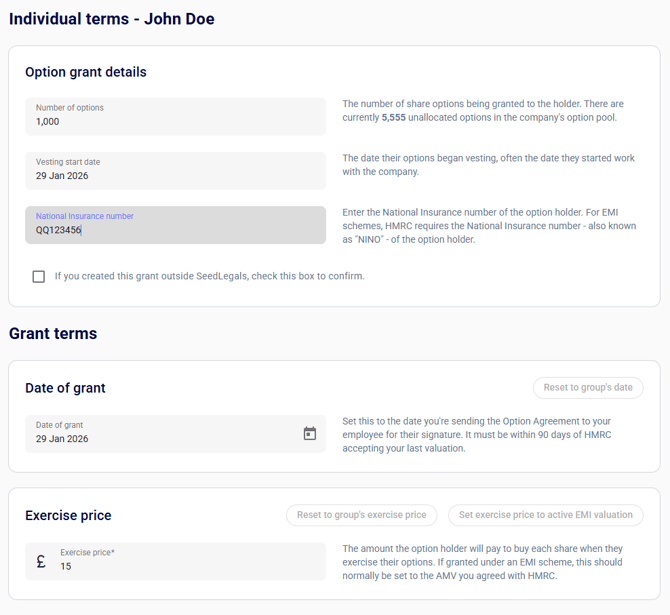

Step 4: Customise Individual Grants (if needed)

You'll now see a list of your option holders. Click the pencil icon next to each person to tailor their specific terms, or leave as it if you’d like the whole group to have the same terms.

For each individual, you'll be able to adjust

- Number of options (how many options they're receiving)

- Vesting start date ie. the date vesting terms begin from

- National Insurance number: this is required for EMI grants, so HMRC can be notified, but will not necessarily be applicable to unapproved grants (eg. an advisor may be based outside of the UK and not have an NI number).

- Grant date: the date the company will sign the Option Agreement (NB. : this is not necessarily the same as the vesting start date)

- Exercise price (see guidance above; for EMI, this is usually the AMV agreed with HMRC)

- Vesting conditions ie. the terms under which the options are earned

Time-based vesting:

If you are setting up an option grant using time-based vesting, you can amend the details of the vesting schedule:

Milestone-based vesting

If you are setting up a milestone-based option grant, you will input the individual milestones and the corresponding number of options which will vest when each milestone has been reached. When setting the milestones, all the options in the grant will need to be accounted for before you can save the grant

Once you’re happy with all the terms of your option grant, please select “Save grant” at the bottom of the page.

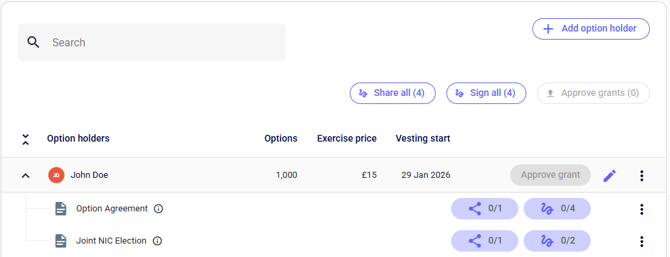

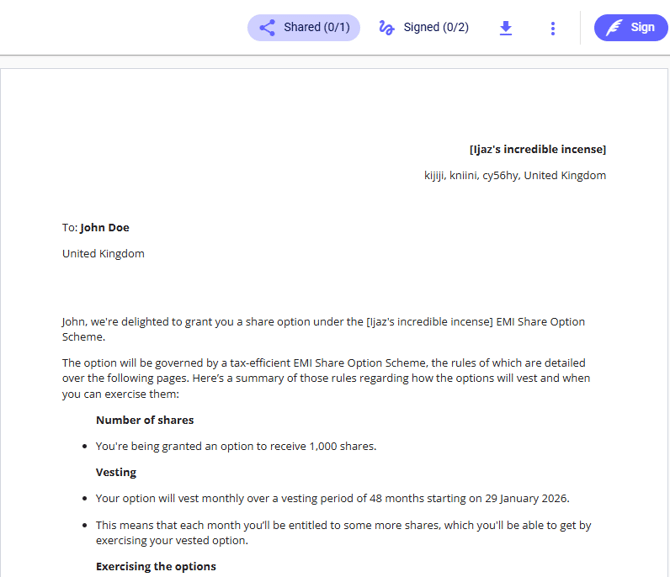

Step 5: Generate and Sign the Option Agreement

Once individual grants are configured, the platform will automatically generate the Option Agreement.

Click on ‘Option Agreement’ to open the document, then hit the blue Sign button to complete it and send it to your option holder's email.

Signing & Witnessing

Because this document is a deed, both the parties will have to have their signatures witnessed, ie. four signatures in total:

For the company:

- Two directors, or

- One director and one person not party to the agreement

For the option holder:

- The option holder

- One person not party to the agreement

The witness must be over 18, not related to the option holder, and not party to the agreement. They must physically watch the holder sign, then sign themselves immediately after, providing their full name and address

Once the document has been signed by the director or option holder, the platform will generate a link to send to your witness.

📺 We have a short video that walks through the signing process — watch it here.

Countersigning deadlines: If your company signs first, the option holder must countersign within 7 or 14 days (depending on your scheme rules).

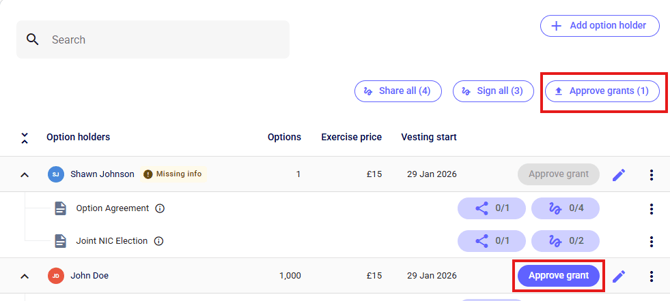

Step 6: Approve the Grant

Once all four signatures are in place, click "Approve Option Grant". This tells the platform the agreement is fully signed, generates an options certificate, and moves the options from available to allocated in the Option Pool.

If you need to complete an NIC Election too, you can do so now — see our guide here.

Step 7: Repeat for All Option Holders

Go through Steps 4–6 for each option holder and wait until all agreements are signed and witnessed.

Don't Forget: HMRC Notification

Once all agreements are completed, you need to notify HMRC:

- EMI grants: You must notify HMRC by 6 July following the end of the tax year. Missing this deadline can cause serious problems, so don't leave it late.

- Unapproved scheme grants (UK employees or directors): No upfront HMRC notification needed, but you must submit an annual notification by 6 July each year for the previous financial year's activity. See our guide here.